1. What is the definition, scope, and significance of the Asia Pacific RTD Alcoholic Beverage Market?

The Asia Pacific Ready‑to‑Drink (RTD) alcoholic beverage market comprises pre‑mixed drinks that combine spirits, flavorings, and carbonated or non‑carbonated bases, packaged for immediate consumption. The scope covers all product categories sold through retail, hospitality, and on‑premise channels across the Asia Pacific region, including major economies such as China, Japan, India, Australia, and Southeast Asian nations. This market is significant because it meets rising consumer demand for convenient, portion‑controlled alcoholic options, drives innovation in flavor and packaging, and contributes substantially to the overall alcoholic beverage industry’s revenue growth.

2. What are the key drivers, restraints, challenges, and opportunities influencing the Asia Pacific RTD Alcoholic Beverage Market?

Key drivers include urbanization, higher disposable incomes, and a growing preference for convenience among younger consumers. Health‑conscious trends encourage low‑calorie and natural‑ingredient formulations, further boosting demand. Restraints involve strict regulatory environments and high excise taxes in several countries, which can limit price competitiveness. Challenges stem from supply‑chain volatility for raw spirits and packaging materials, as well as cultural resistance to alcohol in certain markets. Opportunities arise from premiumization, the introduction of novel flavors, and the expansion of e‑commerce distribution channels, offering avenues for market players to differentiate and capture new segments.

3. What are the current and emerging growth trends shaping the Asia Pacific RTD Alcoholic Beverage Market?

Current trends highlight a shift toward low‑ABV (alcohol by volume) and low‑sugar RTD products, aligning with wellness priorities. Flavour experimentation—such as tropical fruit blends and botanical infusions—appeals to adventurous millennials. Emerging trends include the rise of canned RTDs, which offer portability and sustainability benefits, and the integration of functional ingredients like electrolytes and adaptogens. Additionally, collaborations between spirit brands and local influencers are driving brand visibility and market penetration.

4. How has COVID‑19 impacted the Asia Pacific RTD Alcoholic Beverage Market and what is the recovery trajectory?

The pandemic initially disrupted on‑premise sales as lockdowns closed bars and restaurants, causing a temporary dip in volume. However, strong growth in off‑premise channels—particularly supermarkets, hypermarkets, and online grocery platforms—accelerated the shift toward home consumption. Post‑pandemic, the market has rebounded robustly, with consumer habits favoring convenient at‑home drinking experiences persisting. The recovery trajectory remains positive, supported by pent‑up demand and continued expansion of digital sales channels.

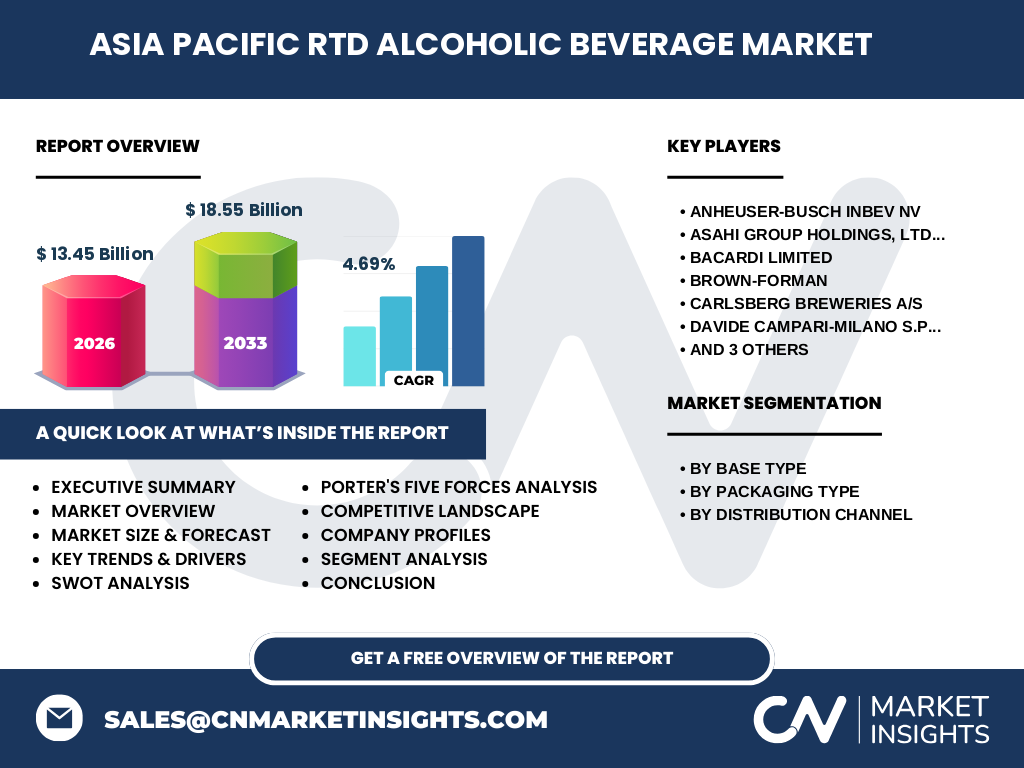

5. Who are the major competitors and what is the level of market consolidation in the Asia Pacific RTD Alcoholic Beverage Market?

The competitive landscape is dominated by global spirits conglomerates and regional brewers. Leading players include Anheuser‑Busch InBev NV, Asahi Group Holdings Ltd., Bacardi Limited, Brown‑Forman, Carlsberg Breweries A/S, Davide Campari‑Milano S.p.A., Diageo plc., Molson Coors Brewing Company, and Suntory Holdings Limited. These companies leverage extensive distribution networks and brand portfolios to capture market share. Consolidation is moderate, with strategic acquisitions and joint ventures enabling firms to broaden product offerings and enter new geographic niches.

6. What are the high‑level overview and key findings of the Asia Pacific RTD Alcoholic Beverage Market?

The market is valued at USD 13.45 billion in 2026 and is projected to reach USD 18.55 billion by 2033, reflecting a CAGR of 4.69 % over the forecast period. Growth is driven by urban lifestyle changes, premiumization, and the surge in low‑calorie options. While regulatory pressures present obstacles, opportunities in innovative packaging and e‑commerce distribution are strong. Competitive dynamics are shaped by a few multinational leaders expanding through product diversification and strategic partnerships.

7. What are the forecast expectations for the Asia Pacific RTD Alcoholic Beverage Market from 2025 to 2032?

Based on the provided CAGR of 4.69 %, the market is expected to continue expanding steadily through 2032. This growth will be underpinned by increasing consumer affinity for convenient, ready‑to‑drink formats, ongoing product innovation, and deeper penetration of digital sales channels. The forecast indicates robust revenue generation, positioning the region as a key growth engine for global RTD players.

8. How is the Asia Pacific RTD Alcoholic Beverage Market sized and shared by segment?

Segmentation by base type includes Whiskey, Rum, Vodka, and Gin, each catering to distinct taste preferences. By packaging, the market is split between bottles and cans, with cans gaining traction for their portability and environmental appeal. Distribution channels are divided among supermarkets & hypermarkets and specialty stores, with the former holding the larger share due to broad consumer reach. Detailed quantitative shares are not disclosed, but the segmentation framework guides strategic focus for brands.

9. What is the geographic distribution of the Asia Pacific RTD Alcoholic Beverage Market size and share?

The market’s geographic footprint spans key sub‑regions: East Asia, Southeast Asia, South Asia, and Oceania. Each sub‑region contributes to the overall USD 13.45 billion valuation, reflecting diverse consumer bases and regulatory landscapes. While exact regional dollar values are not specified, the collective performance of these areas drives the aggregate market size and informs targeted expansion strategies.

10. What are the detailed regional performances within the Asia Pacific RTD Alcoholic Beverage Market?

East Asian markets, led by Japan and South Korea, show strong premium RTD adoption. Southeast Asia, with countries like Thailand, Vietnam, and the Philippines, demonstrates rapid volume growth driven by rising middle‑class consumption. South Asia, particularly India, presents high potential due to a large youthful population and expanding urban centers. Oceania, primarily Australia and New Zealand, contributes stable demand with a penchant for innovative flavor profiles. Each region exhibits unique growth drivers and regulatory nuances.

11. Which companies lead the Asia Pacific RTD Alcoholic Beverage Market and what are their strategic approaches?

Leading firms such as Diageo plc., Bacardi Limited, and Suntory Holdings Limited focus on premium line extensions and localized flavor development. Anheuser‑Busch InBev NV leverages its extensive distribution network to amplify shelf presence. Asahi Group Holdings Ltd. and Carlsberg Breweries A/S prioritize sustainability in packaging, shifting toward recyclable cans. Brown‑Forman and Molson Coors emphasize strategic partnerships with regional bottlers to enhance market penetration. These strategies collectively aim to capture both volume and margin growth.

12. How do Porter’s Five Forces shape the competitive environment of the Asia Pacific RTD Alcoholic Beverage Market?

Threat of new entrants is moderate due to high brand equity requirements and regulatory barriers. Bargaining power of suppliers is relatively low; however, premium spirit sourcing can elevate costs. Bargaining power of buyers is strong, with retailers demanding shelf‑space optimization and promotional support. Threat of substitutes includes traditional on‑premise drinks and emerging non‑alcoholic alternatives, which exert pressure on pricing. Rivalry among existing competitors is intense, driven by continual product launches and marketing spend.

13. What are the SWOT insights for the Asia Pacific RTD Alcoholic Beverage Market?

Strengths: Established brand portfolios, rising consumer convenience demand, and strong distribution channels.

Weaknesses: Sensitivity to regulatory changes and reliance on imported base spirits.

Opportunities: Growth of low‑ABV innovations, canned packaging, and digital sales platforms.

Threats: Increasing excise taxes, health‑focused consumer shifts away from alcohol, and supply‑chain disruptions.

14. How is value created and transferred across the Asia Pacific RTD Alcoholic Beverage Market value chain?

The value chain starts with spirit manufacturers producing base alcohol, followed by formulation experts who blend flavors and adjust ABV. Packaging firms supply bottles or cans, after which bottling partners execute fill‑and‑seal operations. Distribution layers—wholesalers, retailers, and e‑commerce platforms—bring products to consumers. Marketing and brand management add intangible value, while after‑sales data analytics inform future product development.

15. What investment insights can be drawn for stakeholders interested in the Asia Pacific RTD Alcoholic Beverage Market?

Investors should prioritize companies with diversified flavor portfolios and flexible packaging capabilities, as these attributes align with emerging consumer trends. Capital allocation toward brands expanding e‑commerce fulfillment and sustainable packaging can yield higher returns. Partnerships with local bottlers and retailers reduce market entry risk. Monitoring regulatory developments is essential to mitigate fiscal exposure.

16. What are the concluding remarks and key takeaways for the Asia Pacific RTD Alcoholic Beverage Market?

The market is on a steady growth trajectory, underpinned by a 4.69 % CAGR and a projected rise to USD 18.55 billion by 2033. Consumer preferences for convenience, health‑conscious formulations, and innovative packaging drive demand. While regulatory and supply‑chain challenges persist, opportunities in premiumization, digital distribution, and sustainable practices provide a compelling growth narrative for brands and investors alike.

17. How was the research for this market report conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, retailers, and consumer panels, alongside secondary analysis of company filings, trade publications, and government statistics. Data triangulation ensured accuracy, while forecasting utilized historical trend extrapolation aligned with the stated CAGR of 4.69 %.

18. What is the scope of this research and its limitations?

The scope covers the Asia Pacific RTD alcoholic beverage segment across base type, packaging, and distribution channels, focusing on market size, growth, and competitive dynamics up to 2033. Limitations include the absence of granular country‑level revenue breakdowns and the reliance on publicly available data for macro‑economic assumptions.

19. Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Anheuser‑Busch InBev NV, Asahi Group Holdings Ltd., Bacardi Limited, Brown‑Forman, Carlsberg Breweries A/S, Davide Campari‑Milano S.p.A., Diageo plc., Molson Coors Brewing Company, and Suntory Holdings Limited. Recent developments feature Diageo’s launch of low‑calorie canned RTDs in Japan, Bacardi’s partnership with a Southeast Asian e‑commerce platform to expand online sales, and Suntory’s introduction of a premium gin‑based ready‑to‑drink line targeting Australian consumers.